Understanding the Stakes

In the course of building a new customer-focused student loan calculator, MyLoans has come across significant inaccuracies in the Department of Education’s loan simulator, an important financial planning tool for millions of borrowers. These errors are particularly relevant for those with graduate school loans and could have damaging financial consequences. If not corrected, the issue could cost graduate borrowers an estimated $20 billion1 more than what they were quoted over the next 25 years. This blog post aims to shed light on this critical issue, advocating for immediate corrective action to safeguard the financial future of hundreds of thousands of borrowers.

The Role of the Loan Simulator

The loan simulator, hosted on the Department of Education's website, is designed as a pivotal resource for borrowers, offering them a way to calculate and foresee their loan repayment plans. This tool's primary function is to assist borrowers in making informed decisions about their repayment strategies based on their goals. Its importance cannot be overstated, as it guides countless borrowers – a significant portion of the 45 million people with student loans in the U.S. – in planning their financial futures. Accurate simulations are crucial in helping these individuals avoid unforeseen debt and manage their finances effectively.

Identifying the Error

The simulator’s flaw lies in its calculation method. While occasionally it presents the correct results2, often it incorrectly calculates the total cost of the income-based SAVE plan based on only 20 years of payments. In reality, graduate borrowers on the SAVE plan are required to make payments for 25 years3. Consequently, the simulator often erroneously recommends the SAVE plan as the most cost-effective option, when in fact, the real total cost could be substantially higher than shown. This discovery was made through careful comparison of the simulator’s output with standard loan repayment calculations, revealing a persistent pattern of discrepancies for graduate borrowers on the SAVE plan.

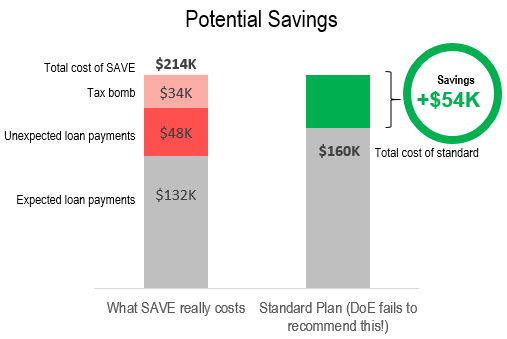

For example, imagine a grad student, Alice, leaving school with $120K in student loans starting a job paying $80K. The Department of Education’s loan tool suggests picking the SAVE plan, costing $132K and ending in 20444. But in truth, using SAVE means paying $180K and finishing in 2049, way more than the standard plan’s $160K (Exhibit A). And that’s not counting the extra ~$30K tax5 hit at forgiveness. While the SAVE plan may make sense for that borrower, depending on their personal circumstances, it should certainly not be presented as the plan with the lowest total amount paid over time.

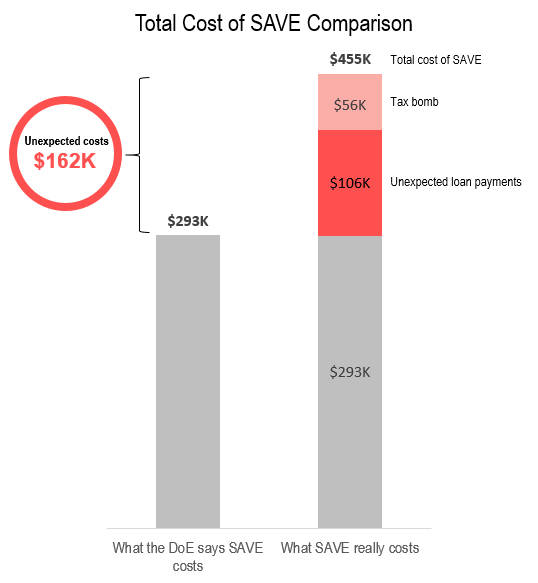

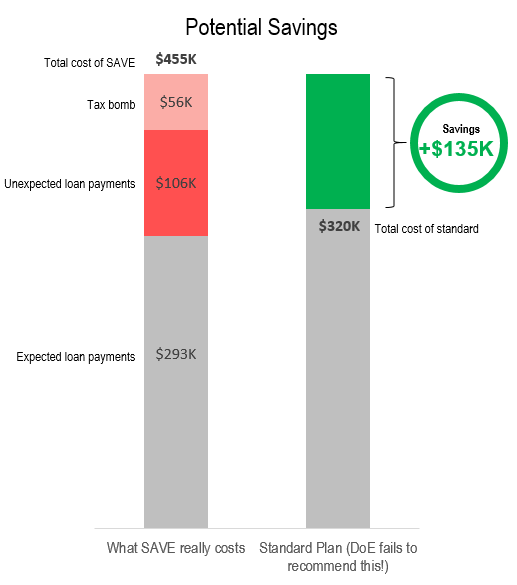

It gets worse for someone with $240K in loans and a $140K salary, let’s call him Bob. The tool says he’d pay $293K, but the real cost is $399K, or $455K with the tax bomb (Exhibit B). All in all, over the life of the loan that’s $82K of unexpected costs for Alice, and $162K of unexpected costs for Bob!

Exhibit A

Exhibit B

Measuring the Impact

The Department of Education's loan simulator error has significant implications for the approximately 12 million Americans with graduate loans, distorting their financial planning. This mistake causes the simulator to often underestimate the cost of the SAVE plan, misleading borrowers into potentially more expensive repayment options. Considering the average graduate borrower has around $80,000 in debt6, the error could result in a $29K misquote7. With 5 million borrowers8 already on the SAVE plan and a considerable portion of federal student loan borrowers being graduate students, the financial misstep amounts to billions of dollars in impact. This error not only affects long-term repayment costs but also borrowers' financial goals, such as saving for retirement or buying a home.

Addressing the Error

Given the significant error in the Department of Education’s loan simulator, we recommend several steps to reduce its effects. Borrowers should verify their loan repayments independently, using tools like our free calculator. If you haven't acted yet, it may be the case that the standard plan is better than the SAVE plan for you9. Alternatively, if you're impacted and you've already signed up for the SAVE plan, then switching is possible and you can save most of the exposure. To be clear, the SAVE plan is certainly a good option for many of borrowers, but not all.

It's also vital to prompt action from the Department of Education to correct this mistake quickly, ensuring the integrity of their resources. Sharing this information widely and contacting representatives can amplify the call for a resolution, helping to safeguard the financial interests of graduate loan borrowers.

Learn More

Ready to take control of your student loans with ease?

Discover How MyLoans Can Help You TodayNo jargon, just clarity